01 // The Story: The ₹50,000 Mistake

(The Hook)

Imagine Arjun. He’s a 30-year-old product manager standing at the checkout counter of an Apple Store in Bangalore. He’s about to buy a MacBook Air for ₹1.2 Lakhs.

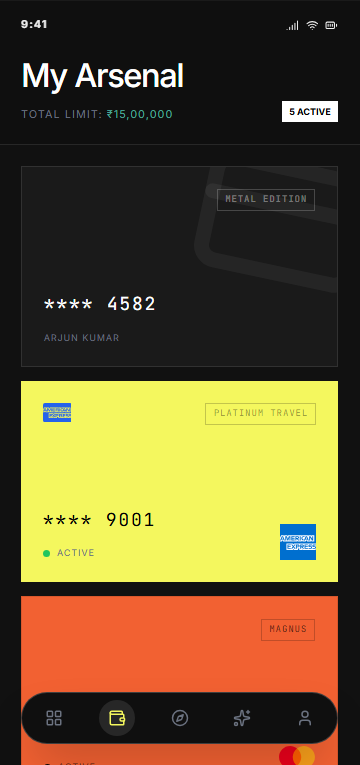

In his leather wallet, he has four premium credit cards: an HDFC Infinia, an Amex Platinum Travel, an Axis Magnus, and a standard SBI Card. He has 10 seconds to make a decision.

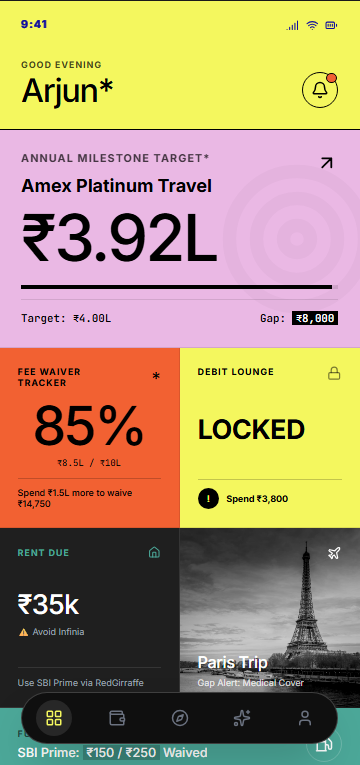

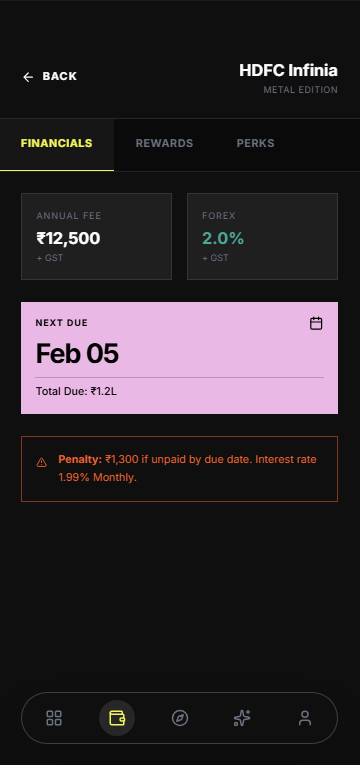

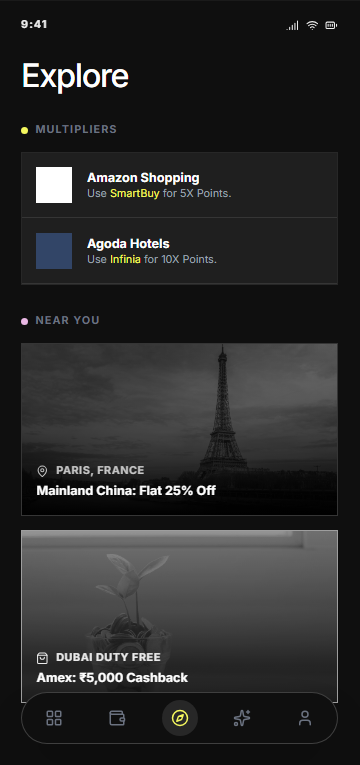

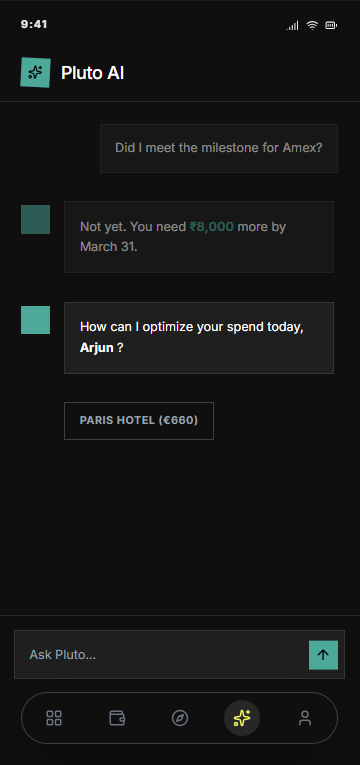

If he swipes the Amex, he hits his ₹4L milestone and gets 40,000 points (worth ₹20k). If he uses the HDFC directly, he gets 3.3% returns. But, if he had bought a Gift Voucher via the HDFC SmartBuy portal 5 minutes ago, he would have received 5X points.

Arjun panics. He swipes the HDFC card directly.

This isn't just Arjun's story. It is the story of every modern Indian consumer facing We treat credit cards like simple payment tools, but the banks have designed them like complex RPG video games. Without a strategy guide, the user always loses.

Pluto is that strategy guide.